Step by step: The steady development of the Spanish market

Spain’s egaming industry has been maturing nicely, but why is it still seen as a poor relation of the European regulated sector?

The Spanish remote gaming market is something of a puzzle. Viewed in a vacuum it’s an undoubted success, with a thriving tightly regulated market full of high-quality operators and strong growth trends.

Online revenues grew by 34% in 2016, on top of 26% growth in the previous year, and all the major operators in the region report positive momentum. And yet, there is the sense that Spain is something of a disappointment.

Total revenues for Spain with a population of nearly 47 million were €420m for 2016, which places it just slightly ahead of the Danish regulated market, where the population is about 12% the size at 5.6 million.

It compares more favourably to Italy, whose 60 million inhabitants generated around €1bn of online gambling revenue in 2016. But by any reasonable metric it’s more famine than feast at the present time.

For long-term industry watchers this wouldn’t have come as a huge surprise. The truism has always been the further south you go in Europe the worse the revenues get. Nonetheless a per capita revenue at around 10% that in the UK and Nordics and around 40% of that generated in Italy is not one that gets euro signs flashing in the eyes of investors, not least because it brings with it a natural cap on the potential number of profitable firms.

If we assume a break-even point of €40m a year in revenues then any operator hoping to turn a profit from Spain would realistically need to grab a minimum of 10% market share. Even assuming a continued 25% growth rate through 2017, which is far from a guarantee, the market would only be €525m at year-end. It suggests a market where only a handful of operators can have any meaningful business and that is how it’s currently playing out.

A recent survey on EGR Intel saw a narrow 58% majority ruling Spain was now too big a market to ignore, but it appears most operators have different views. The list of licensed operators in Spain is by no means short, but it’s fairly limited in terms of those active in the region.

It’s a market dominated by five or six major organisations and almost all of these are ‘foreign’ operators, unlike Italy where the likes of Sisal, SNAI and Lottomatica are all significant players. Major land-based operator Cirsa has a joint-venture with Ladbrokes to operate the Sportium brand in the retail and online sectors. But aside from this it’s bet365, PokerStars, 888, bwin and William Hill which dominate.

In particular bet365 and PokerStars have a stranglehold on the sports betting and poker markets respectively, with PokerStars also rapidly building up scale in the fast growing online casino market. Alongside this we have the well-established bwin brand, and a sizeable Hills business that has developed well from the ex-Sportingbet Miapuesta brand it acquired in 2013.

Hills doesn’t break down its Spanish results, but did note Italy and Spain combined grew by 15% on a local currency basis during 2016 and made a combined operating profit of £1.8m in the period compared to a loss of £400,000 in 2015.

It also noted Spain benefited from an increased product range. And it’s likely the majority of its growth in the period came through Spain as opposed to Italy, where some indicators suggest it has lost market share in recent months.

Slowly slowly

It’s worth noting that Spain is still a very new market. While it has technically been open since mid-2012, it took until 2015 to reach any level of comparable customer offering to the major regulated markets.

The regulator admits that this expansion (which included adding slots and betting exchange products) has been key to its growth in recent years, but arguably more importantly it creates a more sustainable long-term market.

“During the 2013-14 period there was some uncertainty in how successful the regime would be in channelling the gambling consumption towards the regulated offering. But now we are quite confident in the ability of our regime to channel that online gambling consumption,” the regulator said in a recent interview with EGR Intel.

In essence there is the acceptance that the market has only recently come to resemble the finished article. The roll-out of the regulated product set has been intentionally slow and new verticals and sub-verticals have gradually been added to create what is now an example of a truly diverse and open market for consumers.

This has finally created a market operators can happily invest in, although there remains the spectre of punishing tax rates of up to 25%. But the biggest problem remains the size of the market, and it’s difficult to generate excitement in investing in a market with limited potential returns.

Slotting in

To compare it directly with the UK, a growth rate of 10% in the British market would add around £480m during the course of 2017 – an amount larger than the entire Spanish egaming sector. It’s not, therefore, hard to understand why operators are happier to enter a crowded, hugely competitive UK market over the rather less busy Spanish one.

One operator EGR Intel spoke to off the record highlighted the emerging markets of Eastern Europe, Germany, the Nordics and Italy as higher up the list of potential targets right now. But is this underestimating Spain’s potential?

According to the regulator, around 80% of egaming activity in Spain now takes place on regulated sites, which suggests some natural headroom for growth still remaining in the market particularly on the casino side.

“…it’s easy to see Spain’s reinvigorated casino market growing strongly over the next two to three years”

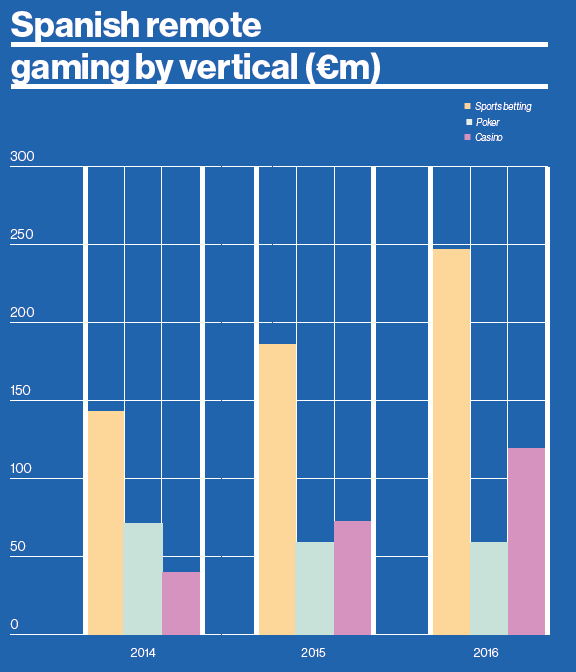

Casino growth in 2016 was electric, rising 73% year-on-year, and was up from 21% to 28% of the total market. While it clearly it benefited from comparisons to a weaker prior year, with slots only introduced in June 2015, the wider trends are interesting.

Casino in nearly every other major market tends to represent a higher overall share of the total revenues generated and it’s easy to see Spain’s reinvigorated casino market growing strongly over the next two to three years. The increasing shift to mobile should also benefit this with cross-sell from the huge sports betting player base a much easier proposition with slick looking 3D slots on the mobile platform.

And crucially for operators looking at entering the market, the casino vertical has always proven far more difficult to dominate than sports or poker, although PokerStars is already looking to stake a major claim here.

Sports betting and poker are perhaps more difficult nuts to crack. The poker market is ruled by PokerStars and 888, with around 60% and 25% market share respectively and it would take a bold firm to try and take either of them on in what are core markets.

Meanwhile in sports betting bet365 is the runaway market leader, which goes in part to explain the dominance of sports betting in total revenues for the Spanish market, with some fierce competition from bwin and William Hill behind them.

That said there are some major brands missing from the market and it would be no surprise to see some of the larger sportsbook operators look to ramp-up their spend and presence in the Spanish market in the coming months.

Yes, currently per capita spend is below almost any other market in Europe but there is no reason to expect it to remain so far behind the curve in the mid-term. Macroeconomic conditions are not as good as in the UK or the Nordics, or even Italy, and expectations of it rising to those levels are fairly unrealistic. But the headroom for growth still seems substantial.

Growth factors

One of the other key factors that could lead to growth is the nature of the player demographics in the Spanish market. Although we’re still waiting for the 2016 updates, the 2015 player data from the regulator paints a picture of a male-dominated market with 83% of active gamblers being men. With a focus to push players into slots from some of the bingo operators, such as the Intertain-owned Botemania, this could be a significant source of new players.

Mobile is also potentially another major growth driver. The Spanish market has lagged behind many of its European cousins in terms of mobile adoption, particularly in terms of iPhone usage with Android a hugely dominant part of the market. The growth of high-quality HTML5 products on mobile web in the gaming sector over the past 12 months can only be beneficial.

There are also some regulatory levers that can still be pulled to increase the size of the market. The most obvious of those is the potential for shared liquidity in poker, which is something the regulator has been working on for some time. Talks continue with the Italian, French and now Portuguese regulators about a shared liquidity pool and it is likely a question of when, not if, this happens.

“We have been working on this for a reasonable time now and it’s something we want to pursue and the most evident and immediate way to do so is by engaging with similar jurisdictions such as Italy, France and Portugal,” the regulator noted.

Cross-border liquidity pooling could give poker a shot in the arm

This would be viewed as a hugely positive change by operators active in Spain. Although there is a danger in assuming this will make too significant a difference to the market, it should at least prevent the slow decline of poker we’ve seen over the past two years.

What could cause a greater investment into the market is a potential reduction in the tax rates. There have been some positive noises from the regulators in Spain, who at least appear to be considering this as an option and not ruling it out from the start, but it feels an unlikely change in the short-term.

With the Netherlands pitching its tax rate even higher than Spain with no shortage of firms looking to enter, it’s hard to make a case its current rate is not at a reasonable level, even if operators may disagree.

Perhaps the best action the regulator is taking, however, is keeping a light touch approach. Advertising has come under more control recently than in previous years, but the intent is still to keep it at a level that drives growth and allows operators to have a profitable sustainable business.

“We have been working over the past two years to regulate gambling advertising, but our initial take is it should be allowed for operators to advertise in an effective and efficient way. The key issue is the protection of minors and we feel we have got the balance right,” the regulator notes.

And yet for all the reasons to be cheerful, it’s hard to get overly excited about the potential of Spain in the near future. It could reasonably become a market worth €500m-plus during the course of 2017, but it’s unlikely we will see a huge influx of new players trying to take advantage of what is still a fairly nascent market.

Instead it’s more likely to remain a small, but meaningful, bottom line contributor to a handful of egaming giants and a market that seems a little more trouble than it’s worth to many others. And that, perhaps, is no small measure of success. The Spanish market works well, just not yet for everyone.