DraftKings and FanDuel – Lies, damned lies, and statistics

In the second of a three-part series, Boom Fantasy CEO Stephen A. Murphy looks underneath the hood at some of the sector's core financial metrics

This is the second part of a three-part series, ‘How the DFS industry almost killed itself (and why it still might).’

I was surprised at how much Part 1 of this series resonated. Vanity metrics are clearly a real (and troubling) phenomenon – in daily fantasy sports and beyond.

Last week, I identified the three big mistakes that the DFS industry has made (and continues to make) – focusing on the wrong metrics, lying about its unit economics, and failing to innovate. Today’s topic: unit economics.

DFS unit economics are simple. How much does it cost to acquire a new depositor? How much value can you generate from that user in her or his lifetime? Customer acquisition cost (CAC) and lifetime value (LTV) are the name of the game in most consumer-facing technology businesses, and it is no different in DFS.

So how did FanDuel and DraftKings screw this up so spectacularly? You don’t raise $1.4bn in venture funding without convincing your investors that you have mind-blowingly positive unit economics, where your LTV is dramatically higher than your CAC and you just need money to scale.

Jason Robins (DraftKings’ CEO) said back in 2015 that the LTV of DraftKings users was upwards of $1,000.

At the time, it cost about $80 to acquire a new DFS depositor. That means Robins was claiming to have in the neighborhood of a 13x LTV:CAC ratio. For some perspective, many investors would salivate at a 3x LTV:CAC ratio. And yet here were a couple companies claiming that they could effectively print money. A few big investors bought what they were selling, many others followed, and they were off to the races.

Here’s what has become the obvious truth – the LTV of a DFS player is nowhere near $1,000. In fact, for too many companies, it isn’t even above CAC.

If it were that high, DraftKings and FanDuel would be rolling in money right now. That is not the case. The reality is that these companies wildly over-estimated their player LTV (or they just gave up caring about it).

So what happened? Did DraftKings and FanDuel lie? Did they mislead? Were they confused? Ignorant? Short of being in the board rooms, I’m not sure who can accurately tell you what was going through their heads.

However, let me offer a guess. My guess is that these companies were omitting critical elements as they calculated and publicly shared their CAC and LTV figures.

Here is how to truly calculate CAC and LTV in the DFS industry.

CAC = paid advertising + upfront deposit bonus + referral payment (if any) + payment processing fee

The lifetime value of a user must not only include the revenue generated, but also subtract the retention and reactivation costs.

LTV = Top-line revenue – overlays – player comps – promotions – payment processing fees – rev share (if any) – retention ads – VIP points – deposit bonuses earned over time

I’d bet dollars to donuts that FanDuel and DraftKings were not including several of these critical elements in their reported LTV and CAC numbers. As a result, they burned through a whole lot of venture capital.

Today, FanDuel and DraftKings are acting more rationally. They still may not have profitable unit economics, but they are spending to survive, not necessarily to expand. However, other companies in the industry are repeating the same mistakes (at a smaller scale).

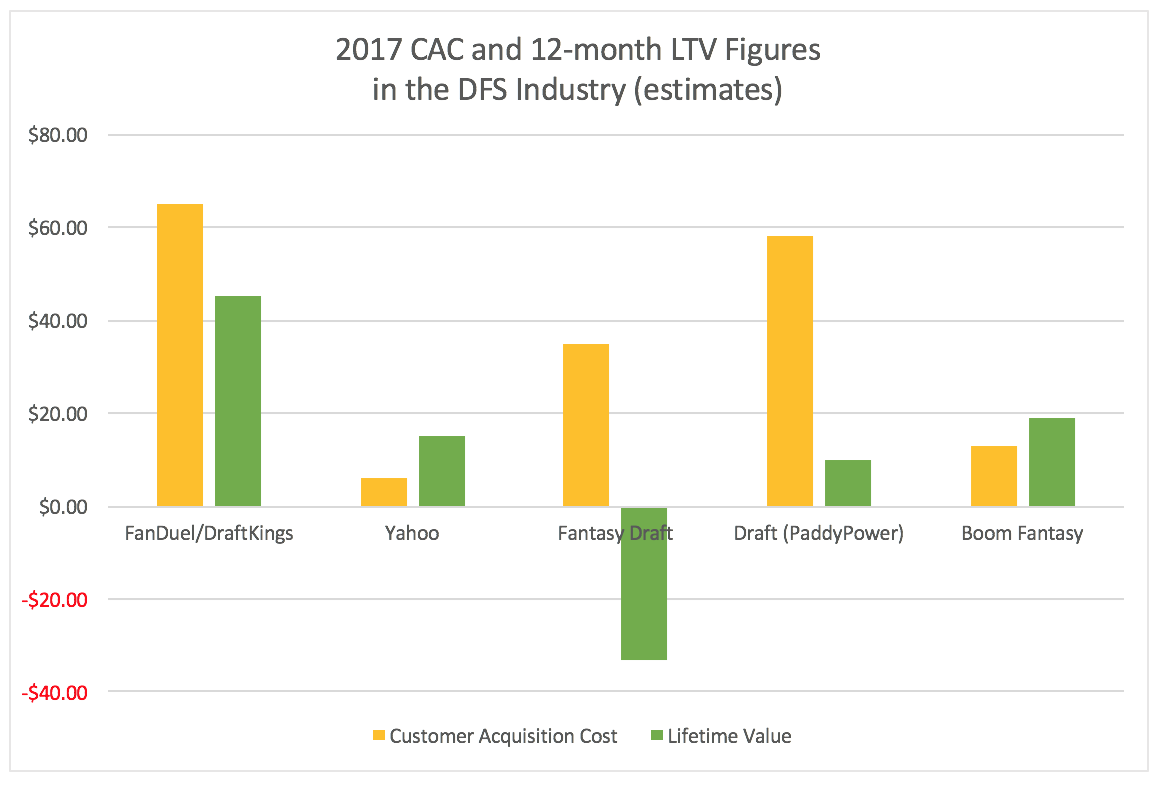

I’m going to provide a very rough estimate of what I think are the true CAC and LTV figures of the major DFS companies in 2017 (using the above definitions). These numbers are not going to be perfect; I don’t have access to any company’s data but my own. But at Boom Fantasy, we track the costs of advertising and affiliate platforms closely and we monitor the overlays and promotions that companies are offering. These figures will be in the right ballpark, although these companies are welcome to share their precise numbers and I will include them in this article.

DraftKings/FanDuel

Estimated CAC: $65

Estimated LTV: $45

So yeah, I’m estimating a $45 LTV, not a $1,000 LTV. Here’s how I got there.

Historically, DraftKings has seen 8 million real-money players. play on its platform. The company has generated less than $500 million in top-line revenue since its founding.

At the very high end, that’s $63 in top-line revenue per user to date ($500 million divided by 8 million). But as we all know by now, top-line revenue does not equal net revenue and it certainly does not equal LTV.

When you factor in that the users they are acquiring in 2017 are less valuable than early adopters, $45 LTV is a reasonable estimate. I’m only estimating the first 12 months of a user’s life, so the total LTV may be higher.

The $65 CAC estimate is far lower than in previous years. At this point, the market leaders are spending less, but are likely still benefiting from all the exposure they generated two years ago.

Yahoo

Estimated CAC: $6

Estimated LTV: $15

Yahoo is spending almost nothing in DFS advertising, leveraging its content and season-long fantasy audience to create a very low effective CAC. Sure, these CAC numbers would increase if Yahoo advertised, but the company has been wise to hold off on mass marketing until it increases LTV.

Fantasy Draft

Estimated CAC: $35

Estimated LTV: -$33

How can you have negative LTV? Lots of overlays and lots of player comps. For a $250-to-enter Fantasy Draft contest, the company gave a buy-one-get-one-free offer for up to 6 entries ($1,500 in free money for any pro). As you see with the LTVs across the industry, these expenses are almost impossible to recover.

Draft (PaddyPower)

Estimated CAC: $58

Estimated LTV: $10

While Draft wisely focused on net revenue pre-acquisition, the company is now making the same mistakes that FanDuel and DraftKings made. The snake draft gameplay – while arguably more fun than salary cap – doesn’t lend itself to high LTVs, as its asynchronous drafting nature and limited multi-entry possibilities prevent users from becoming whales. On top of that, the company has given away close to $400,000 in refunds after suffering technical issues as they scaled, crippling net revenue.

Boom Fantasy

Estimated CAC: $13

Estimated LTV: $19

We are proud of how we have grown our LTV over the past two years, but it is still below the market leaders due to their large prize pools and liquidity. Our CAC is also lower, but that will increase with scale. As a result, we’ve been laser-focused on product and LTV so that we can profitably advertise with scale in the near future.

In conclusion, the LTV numbers of the DFS industry are not what they have been reported to be. These estimates are not precisely accurate, but they are much closer than some of the numbers the industry has been guilty of publicizing.

FanDuel and DraftKings ignored their true unit economics. Draft and Fantasy Draft are making the same mistake today. These decisions are not helping them grow sustainable businesses; they are only contributing to the bottom lines of Facebook and other ad platforms.

In the third and final part of this series, I will discuss innovation and what the industry must do to get these unit economics in the lucrative position that VCs dreamed they could be. It is very possible, but repeating the mistakes of the past won’t get it done.

Stephen A. Murphy is the CEO of Boom Fantasy, a leading pick’em fantasy sports platform that offers a daily $100,000 jackpot. It was named the Best Fantasy Sports Operator of 2017 at the EGR North America Awards. Prior to founding Boom Fantasy, Mr. Murphy was an online gaming consultant for MGM Resorts International, vice president of High 5 Games, and managing editor of Card Player Media.